Python implementation of the ACM Term Premium models

- Nominal version from "Pricing the Term Structure with Linear Regressions" from Adrian, Crump and Moench (2013).

- Real version from "Decomposing Real and Nominal Yield Curves" from Abrahams, Adrian, Crump and Moench (2016).

The NominalACM class prices the time series and cross-section of the term

structure of interest rates using a three-step linear regression approach.

Computations are fast, even with a large number of pricing factors. The object

carries all the relevant variables as atributes:

- The yield curve itself

- The excess returns from the synthetic zero coupon bonds

- The principal components of the curve used as princing factors

- Risk premium parameter estimates

- Yields fitted by the model

- Risk-neutral yields

- Term premium

- Historical in-sample expected returns

- Expected return loadings

The RealACM class extends the nominal model to jointly price nominal and real

(inflation-linked) yield curves. It decomposes nominal yields into expected real

rates, expected inflation, real term premia, inflation risk premia, and a

liquidity premium. The state vector combines nominal PCs, orthogonalized real

PCs, and an observable liquidity factor. Key attributes include:

- Nominal and real model-implied yields (

miy_n,miy_r) - Nominal and real risk-neutral yields (

rny_n,rny_r) - Nominal and real term premia (

tp_n,tp_r) - Breakeven inflation and inflation risk premium (

breakeven,irp) - Forward rate decompositions via

forward_rates_tsandforward_rates_cs

pip install pyacmfrom pyacm import NominalACM

acm = NominalACM(

curve=yield_curve,

n_factors=5,

)The tricky part of using this model is getting the correct data format. The

yield_curve dataframe in the expression above requires:

- Annualized log-yields for zero-coupon bonds

- Observations (index) must be in either monthly or daily frequency

- Maturities (columns) must be equally spaced in monthly frequency and start at month 1. This means that you need to construct a bootstraped curve for every date and interpolate it at fixed monthly maturities

from pyacm import RealACM

acm = RealACM(

nominal_curve=nominal_curve,

real_curve=real_curve,

liquidity=liquidity,

cpi=cpi,

n_factors_n=3,

n_factors_r=2,

selected_maturities_n=[6, 12, 24, 36, 48, 60, 72, 84, 96, 108, 120],

selected_maturities_r=[24, 36, 48, 60, 72, 84, 96, 108, 120],

)In addition to the nominal curve requirements above, the RealACM class needs:

real_curve: annualized log-yields for real (inflation-linked) zero-coupon bonds. Columns must be consecutive integers in monthly maturities (e.g. 24 to 120)liquidity: a positivepd.Serieswith an observable liquidity proxy (e.g. fitting errors, relative trading volumes, or a composite index)cpi: a monthlypd.Serieswith the consumer price index level, used to compute realized inflationselected_maturities_nandselected_maturities_rcontrol which maturities enter the return regressions for the nominal and real curves, respectively

Updated estimates for the US are available on the NY FED website.

The file example_us reproduces the original outputs using the same

dataset as the authors.

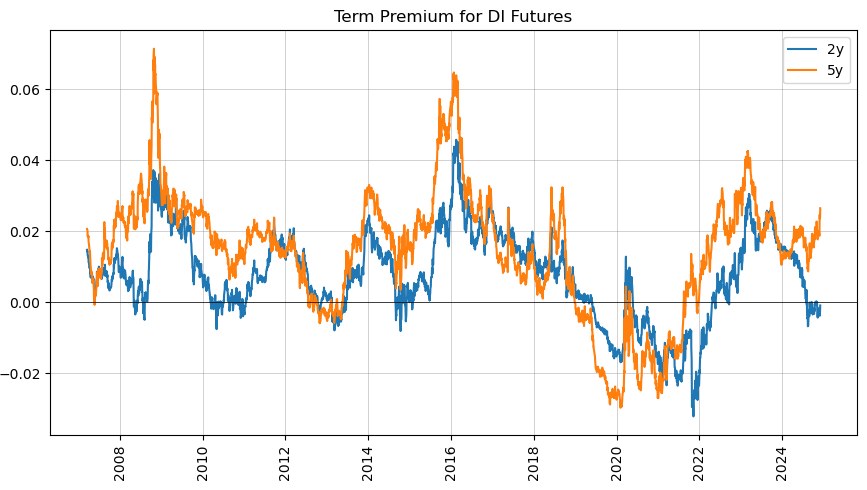

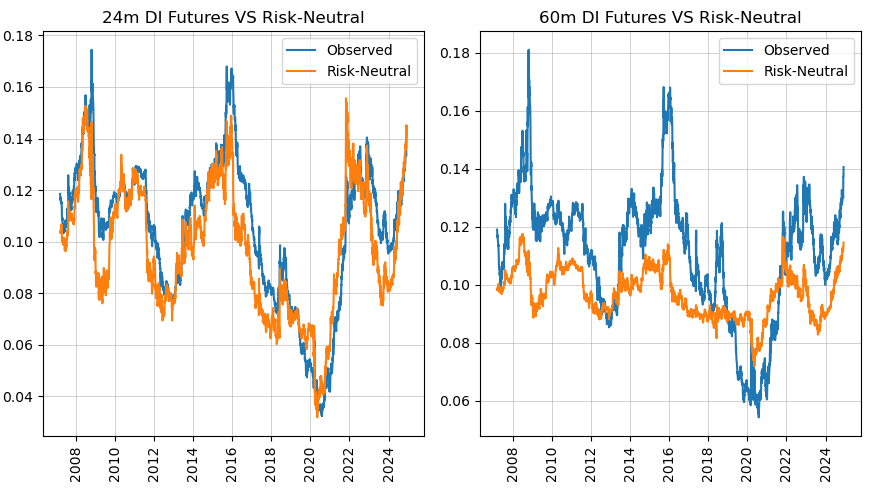

The jupyter notebook example_br

contains an example application to the Brazilian DI futures curve that

showcases all the available methods and attributes.

The file example_real_us

replicates the joint Treasury-TIPS decomposition from Abrahams, Adrian, Crump

and Moench (2016) using US data.

The jupyter notebook example_real_br

applies the RealACM model to Brazilian nominal (LTN/NTN-F) and

inflation-linked (NTN-B) yield curves, decomposing yields into expected real

rates, expected inflation, real term premia, inflation risk premia, and a

liquidity premium.

Adrian, Tobias and Crump, Richard K. and Moench, Emanuel, Pricing the Term Structure with Linear Regressions (April 11, 2013). FRB of New York Staff Report No. 340

Abrahams, Michael and Adrian, Tobias and Crump, Richard K. and Moench, Emanuel, Decomposing Real and Nominal Yield Curves (February, 2015). FRB of New York Staff Report No. 570

I would like to thank Emanuel Moench for sharing his original MATLAB code in order to replicate these results.

Gustavo Amarante (2025). pyacm: Python Implementation of the ACM Term Premium Model. Retrieved from https://github.com/gusamarante/pyacm